The United Arab Emirates (UAE) offers a thriving landscape for import-export businesses, fueled by its strategic location, business-friendly environment, and world-class infrastructure. With over 90% of its GDP attributed to trade, the UAE serves as a global hub for commerce, connecting businesses to markets across Europe, Asia, and Africa. Despite the lucrative opportunities, navigating the regulatory framework and overcoming challenges such as competition, logistical complexities, and cultural barriers require careful planning and strategic partnerships. However, by understanding local laws, building strong relationships, and embracing innovation, import-export businesses can thrive and capitalize on the UAE’s dynamic market to achieve success in the global arena.

Understanding Import Export Business License in UAE

In the bustling landscape of global commerce, the United Arab Emirates (UAE) stands as a beacon of opportunity for importers and exporters alike. With its strategic location, business-friendly policies, and robust infrastructure, the UAE offers an ideal environment for entrepreneurs to thrive in the import-export sector. However, before diving into this lucrative venture, understanding the intricacies of acquiring an import-export business license is paramount.

Import-Export Business License

An import-export business license is a legal document that grants individuals or companies the authority to engage in the buying and selling of goods across international borders. In the UAE, this license is a prerequisite for conducting import-export activities legally and efficiently.

Types of Import-Export Business Licenses in UAE

Commercial License: This license is suitable for businesses involved in importing goods for sale in the local market or exporting products manufactured within the UAE to international markets.

Trading License: A trading license allows businesses to engage in both import and export activities, facilitating a broader scope of operations.

Industrial License: For enterprises involved in manufacturing goods for export, an industrial license is necessary to conduct operations legally.

Professional License: Although primarily for service-oriented businesses, some professional licenses may also encompass import-export activities, depending on the nature of the services offered.

Why is a License Required?

Obtaining an import-export business license in the UAE serves several crucial purposes:

Legal Compliance: Operating without a proper license can result in hefty fines, legal repercussions, and damage to reputation.

Market Credibility: A valid license enhances the credibility of your business in the eyes of customers, suppliers, and regulatory authorities.

Access to Benefits: Licensed businesses are eligible for various incentives, subsidies, and support services provided by the government to promote trade and economic growth.

Process of Obtaining an Import-Export Business License

Acquiring a license to conduct import-export activities in the UAE involves several steps:

Business Setup

Decide on the appropriate legal structure for your business, such as a sole proprietorship, partnership, or company.

Register your business with the relevant authorities, such as the Department of Economic Development (DED) or the relevant free zone authority.

License Application

Determine the type of license required based on your business activities.

Submit the necessary documents, including passport copies, business plan, lease agreement, and other relevant paperwork, to the licensing authority.

Approval Process

Await approval from the licensing authority, which may involve review and verification of submitted documents.

Pay the requisite fees associated with the license application and processing.

Issuance of License

Upon approval, the import-export business license will be issued, enabling you to commence operations legally.

Regulatory Framework for Import-Export Business Licenses in UAE

Understanding Regulatory Authorities

In the UAE, the process of obtaining an import-export business license is governed by various regulatory authorities, depending on the location and nature of the business. Understanding the roles and responsibilities of these authorities is crucial for navigating the licensing process smoothly.

Department of Economic Development (DED)

The DED is responsible for regulating mainland businesses in the UAE.

It oversees the issuance and renewal of commercial licenses for companies operating outside free zones.

Free Zone Authorities

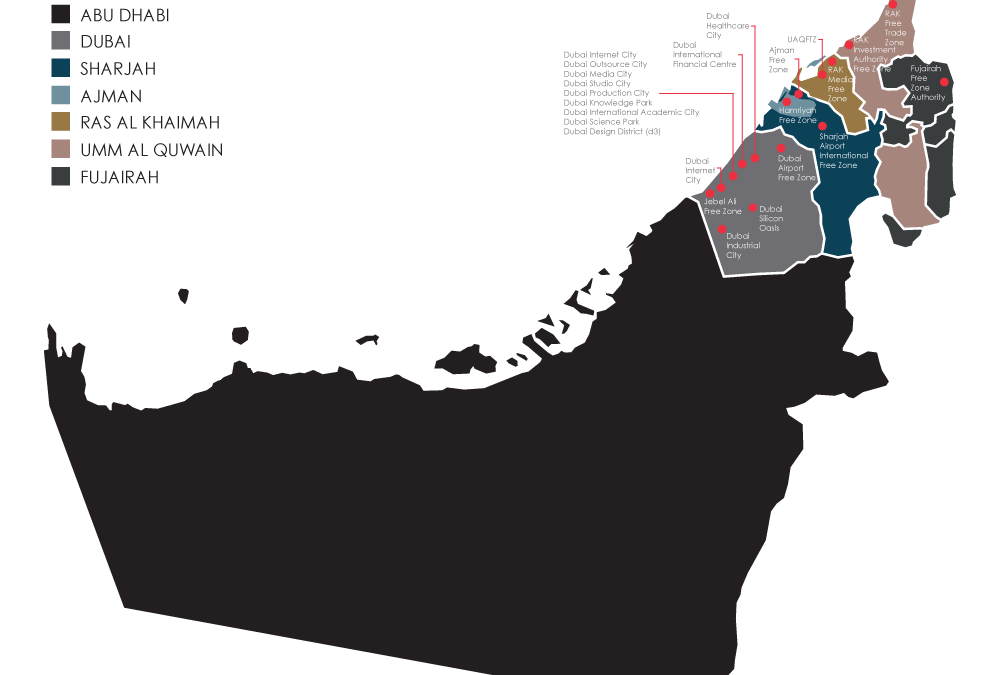

Free zones in the UAE, such as Dubai Airport Free Zone (DAFZA), Jebel Ali Free Zone (JAFZA), and Abu Dhabi Global Market (ADGM), have their own regulatory bodies.

These authorities offer specialized import-export licenses tailored to the needs of businesses operating within the respective free zones.

Customs Authorities

The UAE Federal Customs Authority plays a pivotal role in facilitating international trade by enforcing customs regulations and tariffs.

Businesses must comply with customs requirements and obtain necessary clearances for importing and exporting goods.

Key Requirements for Import-Export Business Licenses

To obtain an import-export business license in the UAE, applicants must fulfill certain criteria and provide essential documentation:

Business Plan

A comprehensive business plan outlining the nature of import-export activities, target markets, marketing strategies, and financial projections is required.

Legal Structure

Applicants must specify the legal structure of their business, whether it is a sole proprietorship, partnership, limited liability company (LLC), or branch of a foreign company.

Proof of Address

Documents verifying the business address, such as lease agreements or ownership deeds, must be submitted as part of the application process.

Trade Name Reservation

Applicants must register a trade name for their business and ensure that it complies with the naming conventions prescribed by the relevant regulatory authority.

Shareholder Details

For companies with multiple shareholders, details of each shareholder, including passport copies and shareholding percentages, must be provided.

Compliance and Regulations

Compliance with relevant regulations and laws is paramount for businesses operating in the import-export sector in the UAE. Key regulations that businesses must adhere to include:

Customs Duties and Tariffs

Businesses must pay applicable customs duties and tariffs on imported and exported goods as per the regulations set by the UAE Federal Customs Authority.

Product Registration and Certification

Certain products may require registration and certification from relevant authorities, such as the Emirates Conformity Assessment Scheme (ECAS) or the Emirates Authority for Standardization and Metrology (ESMA), before they can be imported or exported.

Sanctions and Embargoes

Businesses must ensure compliance with international sanctions and embargoes imposed on specific countries or individuals to avoid legal repercussions.

Benefits and Challenges of Operating an Import-Export Business in UAE

Unlocking Opportunities in a Global Hub

The United Arab Emirates (UAE) serves as a dynamic gateway to international trade, offering a myriad of opportunities for import-export businesses. Let’s explore the benefits and challenges associated with operating in this vibrant market:

Benefits of Operating in UAE

Strategic Location: Situated at the crossroads of Europe, Asia, and Africa, the UAE provides easy access to major global markets, facilitating efficient trade routes and logistics.

Business-Friendly Environment: With its liberal economic policies, tax incentives, and free zones, the UAE offers a conducive environment for businesses to thrive and expand their operations.

Infrastructure and Connectivity: The UAE boasts world-class infrastructure, including modern ports, airports, and logistics facilities, ensuring smooth transportation and distribution of goods.

Diverse Market Opportunities: The UAE’s diverse population and cosmopolitan culture create a robust consumer market, offering a wide range of opportunities for businesses to tap into various industries and sectors.

Challenges Faced by Import-Export Businesses

Regulatory Complexity: Navigating the regulatory landscape can be challenging, with multiple authorities involved in licensing, customs clearance, and compliance requirements.

Competition: The UAE’s attractiveness as a business hub also means high competition in the import-export sector, requiring businesses to differentiate themselves through innovation, quality, and market positioning.

Cultural and Language Barriers: Doing business in the UAE requires understanding and navigating cultural norms and language barriers, particularly in communication and negotiation with local partners and stakeholders.

Logistical Challenges: Despite its advanced infrastructure, import-export businesses may encounter logistical challenges such as congestion at ports, customs delays, and transportation bottlenecks.

Tips for Success in UAE’s Import-Export Sector

To overcome challenges and maximize opportunities in the UAE’s import-export sector, consider the following tips:

Understand Local Laws and Regulations

Thoroughly research and understand the legal and regulatory requirements governing import-export activities in the UAE to ensure compliance and avoid penalties.

Build Strong Partnerships

Cultivate relationships with reliable suppliers, distributors, and logistics partners in the UAE to streamline operations and enhance market reach.

Invest in Technology and Innovation

Leverage technology solutions for supply chain management, logistics optimization, and market intelligence to stay competitive and agile in the rapidly evolving business landscape.

Focus on Quality and Differentiation

Emphasize product quality, innovation, and value-added services to differentiate your offerings and stand out in the competitive market.

Stay Agile and Adaptive

Remain flexible and adaptive to market changes, emerging trends, and geopolitical developments to seize new opportunities and mitigate risks effectively.

Conclusion:

In conclusion, establishing an import-export business in the United Arab Emirates presents both opportunities and challenges. The UAE’s strategic location, business-friendly policies, and robust infrastructure make it an attractive destination for international trade. However, navigating the regulatory landscape, competition, and logistical hurdles require careful planning, adherence to regulations, and strategic partnerships. By leveraging the UAE’s advantages, staying abreast of market trends, and adopting innovative approaches, import-export businesses can thrive and capitalize on the vast potential of this dynamic market. With commitment, perseverance, and a strategic mindset, entrepreneurs can unlock the full potential of the UAE as a gateway to global trade and prosperity.

1. What types of import-export business licenses are available in the UAE?

Answer: The UAE offers various types of import-export licenses, including commercial, trading, industrial, and professional licenses, tailored to different business activities.

2. How do I apply for an import-export business license in the UAE?

Answer: To apply for a license, you need to determine the type of license required, submit necessary documents to the relevant authority, await approval, and pay the required fees upon issuance.

3. What documents are needed to apply for an import-export business license in the UAE?

Answer: Required documents typically include passport copies, business plan, lease agreement, trade name reservation, and shareholder details, among others.

4. Are there specific regulations for importing and exporting goods in the UAE?

Answer: Yes, businesses must comply with customs regulations, tariffs, product registration, and certification requirements enforced by the UAE Federal Customs Authority and other relevant authorities.

5. What are the benefits of operating an import-export business in the UAE?

Answer: Benefits include the UAE’s strategic location, business-friendly environment, diverse market opportunities, and world-class infrastructure facilitating efficient trade routes.

6. How can I overcome competition in the UAE’s import-export sector?

Answer: Differentiate your offerings through quality, innovation, and value-added services, while also building strong partnerships and staying agile to adapt to market changes.

7. What challenges do import-export businesses face in the UAE?

Answer: Challenges include regulatory complexity, competition, logistical hurdles, and cultural and language barriers requiring careful planning and strategic approaches.

8. Is it necessary to register a trade name for an import-export business in the UAE?

Answer: Yes, registering a trade name is essential for branding and legal purposes, and it must comply with naming conventions prescribed by the relevant regulatory authority.

9. Are there specific incentives available for import-export businesses in the UAE?

Answer: Yes, import-export businesses may be eligible for incentives, subsidies, and support services provided by the government to promote trade and economic growth.

10. How important is compliance with local laws and regulations for import-export businesses in the UAE?

Answer: Compliance is crucial to avoid fines, legal repercussions, and damage to reputation, as well as to gain market credibility and access to benefits.

11. Can foreign companies establish import-export businesses in the UAE?

Answer: Yes, foreign companies can establish import-export businesses in the UAE by registering with the relevant authorities and fulfilling legal requirements.

12. What role do free zones play in the import-export sector in the UAE?

Answer: Free zones offer specialized import-export licenses and incentives, providing businesses with a conducive environment for trade and investment.

13. How can technology be leveraged to enhance import-export operations in the UAE?

Answer: Technology solutions can streamline supply chain management, optimize logistics, and provide market intelligence, enhancing competitiveness and efficiency.

14. Are there specific regulations regarding customs duties and tariffs for imported and exported goods in the UAE?

Answer: Yes, businesses must adhere to customs duties and tariffs set by the UAE Federal Customs Authority, which vary based on the nature of the goods and trade agreements.

15. What steps can businesses take to ensure success in the import-export sector in the UAE?

Answer: Businesses should understand local laws, build strong partnerships, invest in technology and innovation, focus on quality and differentiation, and remain agile and adaptive to market changes.

In summary, establishing a business in a UAE free zone presents lucrative opportunities for entrepreneurs seeking to tap into the dynamic Middle Eastern market. With over 45 free zones catering to diverse industries, investors can benefit from advantages such as 100% foreign ownership, tax exemptions, and customs duty benefits. By carefully selecting the right free zone jurisdiction, determining the appropriate business activities and legal structure, and gathering the necessary documentation, entrepreneurs can initiate the setup process. However, it’s crucial to understand and adhere to the regulatory framework, including company laws, visa and immigration requirements, and compliance obligations. Seeking professional assistance can streamline the setup process and ensure compliance, ultimately enabling entrepreneurs to capitalize on the UAE’s business-friendly environment and strategic location for global expansion.

Understanding the Basics of UAE Free Zones

In recent years, the United Arab Emirates (UAE) has emerged as a thriving hub for businesses seeking lucrative opportunities in the Middle East. With its strategic location, business-friendly environment, and robust infrastructure, the UAE offers entrepreneurs a range of options to establish their ventures. One of the most popular choices among foreign investors is setting up a business in a UAE free zone.

UAE Free Zones

UAE free zones are designated areas within the country that offer foreign investors numerous benefits and incentives to establish their businesses. These zones are designed to attract foreign investment, promote economic diversification, and foster innovation across various sectors. Each free zone in the UAE is governed by its own set of regulations and authorities, providing investors with flexibility and autonomy in managing their enterprises.

Advantages of Setting Up in a Free Zone

100% Foreign Ownership: One of the primary advantages of establishing a business in a UAE free zone is that foreign investors can own their companies entirely, without the need for local sponsorship or partnership.

Tax Exemption: Companies operating within free zones are typically exempt from corporate and income taxes for a specified period, usually ranging from 15 to 50 years, depending on the jurisdiction.

Customs Duty Benefits: Businesses in free zones enjoy customs duty exemptions on imports and exports, facilitating seamless international trade.

Simplified Business Setup: The process of setting up a company in a UAE free zone is streamlined and efficient, with minimal bureaucratic hurdles and paperwork requirements.

Strategic Location: Many free zones in the UAE are strategically located near major seaports, airports, and business hubs, providing convenient access to global markets.

Types of Free Zone Entities

Before diving into the requirements for setting up a business in a UAE free zone, it’s essential to understand the different types of entities available to investors.

Free Zone Company (FZCO)

A Free Zone Company, also known as an FZCO, is a legal entity with multiple shareholders. These companies can be formed with a minimum of two shareholders and a maximum of five.

Free Zone Establishment (FZE)

A Free Zone Establishment, or FZE, is a single-shareholder company. Unlike an FZCO, which requires multiple shareholders, an FZE can be owned entirely by a single individual or corporate entity.

Branch Office

Foreign companies looking to establish a presence in the UAE without setting up a separate legal entity can opt to open a branch office in a free zone. Branch offices operate as extensions of their parent companies and are subject to the regulations of the free zone authority.

Requirements for Setting Up a Business in UAE Free Zones

Establishing a business in a UAE free zone requires careful planning, thorough research, and adherence to specific guidelines set forth by the respective free zone authorities. Whether you’re a budding entrepreneur or an established company looking to expand into the UAE market, understanding the requirements is crucial for a smooth and successful setup process.

Choose the Right Free Zone

The first step in setting up a business in a UAE free zone is selecting the most suitable jurisdiction for your enterprise. With over 45 free zones across the country, each catering to specific industries and business activities, it’s essential to research and identify the zone that aligns with your business objectives.

Factors to Consider:

Industry Focus: Different free zones specialize in various sectors such as technology, media, healthcare, logistics, and more. Choose a zone that caters to your industry.

Location: Consider the proximity to key infrastructure, transportation hubs, and target markets when selecting a free zone location.

License Types: Free zones offer different types of licenses based on business activities. Ensure the chosen zone provides the necessary license for your operations.

Determine Business Activity and Legal Structure

Once you’ve chosen the free zone, you’ll need to determine the specific business activities you intend to undertake and select an appropriate legal structure for your company.

Common Business Activities:

Trading

Consulting

Manufacturing

Service provision

E-commerce

Legal Structures Available:

Free Zone Company (FZCO)

Free Zone Establishment (FZE)

Branch Office

Gather Required Documents

Before initiating the company setup process, gather all the necessary documents as per the requirements of the chosen free zone. While the exact documentation may vary depending on the jurisdiction and business activity, the following are commonly required:

Passport copies of shareholders and directors

Proof of address for shareholders and directors

Business plan

Memorandum and Articles of Association (for FZCO and FZE)

No Objection Certificate (if applicable)

Power of Attorney (if applicable)

Secure Office Space and Trade Name

Most free zones require businesses to lease office space within the designated area. Additionally, you’ll need to register a unique trade name for your company, ensuring it complies with the naming guidelines specified by the free zone authority.

Tips:

Consult with the free zone authority to understand office space requirements and lease agreements.

Conduct a trade name availability check to ensure your desired name is not already in use.

Apply for License and Company Registration

Once you have all the necessary documents and office space secured, you can proceed to apply for the business license and company registration through the respective free zone authority.

Process Overview:

Submit the application form along with required documents.

Pay the applicable fees for license issuance and registration.

Await approval from the free zone authority, which typically takes a few days to a few weeks, depending on the jurisdiction.

Additional Considerations and Best Practices

Setting up a business in a UAE free zone is an exciting endeavor that offers numerous opportunities for growth and expansion. However, there are several additional considerations and best practices to keep in mind to ensure a successful venture.

Understand Regulatory Framework

Before proceeding with company formation, it’s essential to familiarize yourself with the regulatory framework governing business activities within the chosen free zone. Each free zone has its own set of rules, regulations, and compliance requirements that businesses must adhere to.

Key Regulations to Consider:

Company Law: Understand the laws and regulations governing company formation, corporate governance, and shareholder rights.

Visa and Immigration: Familiarize yourself with visa and immigration regulations for employees and shareholders, including residency permits and work visas.

Taxation: While free zones offer tax exemptions, it’s crucial to stay informed about any changes to tax laws and regulations that may impact your business in the future.

Consider Visa and Immigration Requirements

If you plan to relocate to the UAE or hire foreign employees for your business, you’ll need to navigate the visa and immigration process. Most free zones offer visa sponsorship services, allowing businesses to apply for residence visas and work permits for their employees.

Visa Types:

Investor Visa: Available for company owners and shareholders.

Employee Visa: Required for foreign employees working in the company.

Dependent Visa: Allows family members of visa holders to reside in the UAE.

Banking and Financial Services

Setting up a business bank account is a crucial step in managing your company’s finances and facilitating transactions. Choose a reputable bank with a presence in the UAE and inquire about the requirements for opening a corporate bank account in the chosen free zone.

Considerations:

Bank Account Opening Requirements: Provide the necessary documentation and comply with anti-money laundering (AML) regulations.

Online Banking Services: Look for banks that offer convenient online banking platforms for seamless financial management.

Compliance and Reporting Obligations

Once your business is up and running, it’s important to stay compliant with the regulations set forth by the free zone authority. This includes filing annual reports, renewing licenses, and fulfilling any other compliance obligations as required.

Compliance Checklist:

Annual Audit: Some free zones may require companies to conduct annual audits by approved auditors.

License Renewal: Ensure timely renewal of your business license to avoid penalties or suspension of operations.

Financial Reporting: Maintain accurate financial records and submit reports as per the free zone regulations.

Seek Professional Assistance

Navigating the intricacies of setting up a business in a UAE free zone can be daunting, especially for first-time entrepreneurs. Consider seeking professional assistance from legal advisors, business consultants, or company formation experts who specialize in free zone setups.

Benefits of Professional Assistance:

Expert Guidance: Receive personalized guidance and support throughout the setup process.

Compliance Assurance: Ensure compliance with all legal and regulatory requirements.

Time and Cost Savings: Streamline the setup process and avoid costly mistakes.

Conclusion:

In conclusion, setting up a business in a UAE free zone offers a gateway to thriving opportunities in the heart of the Middle East. With favorable incentives like 100% foreign ownership and tax exemptions, coupled with streamlined setup processes, entrepreneurs can establish their ventures with ease. However, success in the UAE free zone landscape requires thorough research, compliance with regulations, and strategic decision-making. By understanding the nuances of the chosen free zone, navigating visa and immigration requirements, and embracing professional assistance when needed, entrepreneurs can position themselves for sustainable growth and prosperity. As the UAE continues to solidify its reputation as a global business hub, seizing the advantages of free zone establishments presents an exciting path towards realizing entrepreneurial dreams in a dynamic and vibrant market.

FAQs:

What is a UAE free zone?

A UAE free zone is a designated area within the country that offers foreign investors various benefits and incentives to establish their businesses, such as 100% foreign ownership, tax exemptions, and customs duty benefits.

How many free zones are there in the UAE?

There are over 45 free zones in the UAE, each catering to specific industries and business activities.

What are the advantages of setting up a business in a UAE free zone?

The advantages include 100% foreign ownership, tax exemptions, customs duty benefits, simplified business setup processes, and strategic location near major transportation hubs.

What types of businesses can be set up in UAE free zones?

Businesses across various sectors such as trading, consulting, manufacturing, services, and e-commerce can be established in UAE free zones.

Do I need a local sponsor to set up a business in a UAE free zone?

No, foreign investors can own their companies entirely in UAE free zones without the need for a local sponsor.

What are the different types of legal structures available for businesses in UAE free zones?

The main legal structures include Free Zone Company (FZCO), Free Zone Establishment (FZE), and Branch Office.

What documents are required to set up a business in a UAE free zone?

Required documents typically include passport copies of shareholders and directors, proof of address, business plan, memorandum and articles of association, and any applicable certificates or permits.

How long does it take to set up a business in a UAE free zone?

The setup process can vary depending on the chosen free zone and the type of business, but it generally takes a few days to a few weeks.

What are the visa requirements for setting up a business in a UAE free zone?

Most free zones offer visa sponsorship services for investors and employees, allowing them to obtain residency permits and work visas.

Can I operate outside the UAE from a free zone company?

Free zone companies can conduct business internationally, but there may be restrictions or additional requirements depending on the jurisdiction.

Are there any restrictions on hiring employees for a business in a UAE free zone?

Free zone companies can hire both local and foreign employees, but they must comply with labor laws and regulations set by the free zone authority.

Do I need to rent office space in a UAE free zone?

Yes, most free zones require businesses to lease office space within the designated area as part of the setup process.

What are the annual compliance requirements for businesses in UAE free zones?

Annual compliance requirements may include renewing business licenses, conducting audits, submitting financial reports, and fulfilling any other obligations set by the free zone authority.

Can I transfer my existing business to a UAE free zone?

Yes, it is possible to transfer an existing business to a UAE free zone, but the process and requirements may vary depending on the jurisdiction and the type of business.

Are there any restrictions on the repatriation of profits from a business in a UAE free zone?

Generally, there are no restrictions on the repatriation of profits from a business in a UAE free zone, but it’s essential to comply with any applicable foreign exchange regulations and reporting requirements.

In summary, the United Arab Emirates (UAE) has established a robust Anti-Money Laundering (AML) framework to combat financial crimes effectively. With its bustling financial centers in Dubai and Abu Dhabi, the UAE recognizes the importance of upholding integrity and transparency in its financial sector. The regulatory framework, including Federal Decree-Law No. 20 of 2018, imposes stringent obligations on financial institutions to prevent money laundering activities. Key measures such as Know Your Customer (KYC) procedures, transaction monitoring, and employee training are integral to AML compliance. However, challenges such as evolving regulatory requirements, cybersecurity risks, and the emergence of new technologies persist. Collaborative efforts, both domestically and internationally, are essential for addressing these challenges and staying ahead of evolving threats. Through proactive measures and strategic investments in technology and compliance, the UAE remains committed to maintaining its reputation as a global financial hub while safeguarding against money laundering activities.

Understanding Anti-Money Laundering (AML) in the UAE

In an era where financial crimes pose significant threats to global economies, jurisdictions worldwide are fortifying their regulatory frameworks to combat illicit financial activities effectively. The United Arab Emirates (UAE), renowned for its bustling financial centers in Dubai and Abu Dhabi, stands at the forefront of this battle against money laundering. Understanding the nuances of Anti-Money Laundering (AML) in the UAE is crucial for businesses and individuals alike to navigate the financial landscape securely.

Anti-Money Laundering (AML)

Anti-Money Laundering refers to a set of regulations, laws, and procedures designed to prevent criminals from disguising illegally obtained funds as legitimate income. The primary aim is to deter illicit activities such as drug trafficking, terrorism financing, corruption, and tax evasion by implementing robust measures within financial systems.

The Importance of AML in the UAE

The UAE, with its rapidly growing economy and international financial hubs, recognizes the critical importance of combating money laundering activities. As a global financial center, the UAE’s commitment to upholding the highest standards of integrity and transparency is paramount to maintaining its reputation and fostering investor confidence.

Regulatory Framework

The UAE has enacted comprehensive legislation and established regulatory bodies to combat money laundering effectively. The Central Bank of the UAE serves as the primary regulatory authority overseeing financial institutions’ compliance with AML regulations. Additionally, the Financial Intelligence Unit (FIU) operates under the umbrella of the UAE Ministry of Justice, responsible for receiving and analyzing suspicious transaction reports.

Legal Framework

The legal framework governing AML efforts in the UAE is robust and multifaceted. The Federal Decree-Law No. 20 of 2018 concerning anti-money laundering and combating the financing of terrorism (AML/CFT) outlines the obligations and responsibilities of entities operating within the UAE’s financial sector. Furthermore, the UAE’s Penal Code imposes severe penalties for individuals found guilty of money laundering offenses.

Role of Financial Institutions

Financial institutions play a pivotal role in the AML landscape of the UAE. Banks, investment firms, insurance companies, and other financial service providers are required to implement stringent Know Your Customer (KYC) procedures to verify the identity of their clients and assess the legitimacy of their transactions. Moreover, these institutions are obligated to monitor customer transactions diligently and report any suspicious activities to the relevant authorities.

International Cooperation

Recognizing the transnational nature of financial crimes, the UAE actively participates in international efforts to combat money laundering and terrorism financing. The country collaborates with various international organizations, including the Financial Action Task Force (FATF), to strengthen its AML/CFT regime and exchange information with foreign counterparts.

Implementing AML Measures in the UAE

Now that we have a foundational understanding of Anti-Money Laundering (AML) in the UAE, it’s essential to delve deeper into the practical implementation of AML measures within the country’s financial landscape. From stringent compliance requirements to technological innovations, various strategies are employed to mitigate the risks associated with money laundering activities.

Compliance Requirements

Financial institutions operating in the UAE are subject to strict compliance requirements mandated by regulatory authorities. These requirements include conducting thorough due diligence on customers, monitoring transactions for suspicious activities, and maintaining comprehensive records of financial transactions. Non-compliance with these regulations can result in severe penalties, including fines and license revocation.

Know Your Customer (KYC) Procedures

One of the cornerstones of AML efforts in the UAE is the implementation of robust Know Your Customer (KYC) procedures. Financial institutions are required to verify the identity of their customers, assess their risk profiles, and obtain sufficient information to understand the nature of their business activities. This ensures that institutions can identify and mitigate the risks associated with potential money laundering activities.

Customer Due Diligence (CDD)

In addition to KYC procedures, financial institutions are also required to conduct Customer Due Diligence (CDD) to assess the integrity of their clients and the legitimacy of their transactions. Enhanced due diligence measures are applied to high-risk customers, such as politically exposed persons (PEPs) and entities operating in high-risk jurisdictions, to mitigate the elevated risks associated with these relationships.

Transaction Monitoring

Transaction monitoring plays a crucial role in detecting and preventing money laundering activities in the UAE. Financial institutions utilize sophisticated monitoring systems and algorithms to analyze customer transactions in real-time, flagging any unusual or suspicious activities for further investigation. This proactive approach enables institutions to identify potential instances of money laundering and take appropriate action promptly.

Training and Awareness Programs

To ensure effective implementation of AML measures, financial institutions invest in comprehensive training and awareness programs for their employees. Training sessions cover various topics, including AML regulations, red flag indicators of suspicious activities, and reporting obligations. By equipping employees with the knowledge and skills necessary to identify and report potential money laundering activities, institutions strengthen their overall AML compliance posture.

Technological Innovations

Advancements in technology have revolutionized AML efforts in the UAE, enabling financial institutions to leverage sophisticated tools and systems to enhance their detection capabilities. Artificial intelligence (AI), machine learning, and data analytics play pivotal roles in identifying patterns and anomalies indicative of money laundering activities. Additionally, blockchain technology is being explored as a means to enhance transparency and traceability in financial transactions.

Challenges and Future Trends in AML in the UAE

While the UAE has made significant strides in strengthening its Anti-Money Laundering (AML) framework, several challenges persist, and emerging trends shape the future landscape of AML efforts in the country. From evolving regulatory requirements to technological advancements, staying ahead of the curve is essential to effectively combatting financial crimes.

Regulatory Challenges

The evolving nature of financial crimes and the global regulatory landscape present ongoing challenges for AML efforts in the UAE. Regulatory requirements are subject to frequent updates and revisions, necessitating continuous monitoring and adaptation by financial institutions to ensure compliance. Additionally, inconsistencies in AML regulations across jurisdictions can create compliance complexities for multinational institutions operating in the UAE.

Cybersecurity Risks

As financial transactions increasingly migrate to digital platforms, the risk of cyber-enabled money laundering poses a significant threat to the UAE’s financial sector. Cybercriminals exploit vulnerabilities in financial systems to launder illicit funds through online channels, highlighting the importance of robust cybersecurity measures to safeguard against such threats. Financial institutions must invest in cybersecurity infrastructure and implement stringent protocols to mitigate the risk of cyber-enabled money laundering.

Emerging Technologies

The rapid pace of technological innovation introduces both opportunities and challenges for AML efforts in the UAE. While technologies such as artificial intelligence (AI), machine learning, and blockchain hold immense potential for enhancing detection capabilities and improving transaction transparency, they also present novel risks and complexities. Financial institutions must strike a balance between harnessing the benefits of emerging technologies and mitigating associated risks through effective risk management and regulatory compliance.

Cross-Border Collaboration

Given the transnational nature of financial crimes, effective cross-border collaboration is essential for combating money laundering effectively. The UAE actively engages in international cooperation initiatives and information sharing agreements to facilitate the exchange of financial intelligence and enhance coordination with foreign counterparts. Strengthening collaborative efforts at the regional and global levels is paramount to addressing the evolving threats posed by money laundering activities.

Enhanced Data Analytics

Data analytics plays a pivotal role in AML efforts, enabling financial institutions to leverage vast amounts of data to identify patterns, trends, and anomalies indicative of money laundering activities. Advanced data analytics tools empower institutions to enhance their risk assessment capabilities, improve transaction monitoring accuracy, and streamline compliance processes. As data analytics technologies continue to evolve, financial institutions in the UAE must invest in data-driven approaches to strengthen their AML compliance frameworks.

In conclusion, Anti-Money Laundering (AML) efforts in the United Arab Emirates (UAE) represent a multifaceted approach aimed at safeguarding the integrity of its financial sector. Through comprehensive regulatory frameworks, stringent compliance requirements, and proactive measures such as Know Your Customer (KYC) procedures and transaction monitoring, the UAE strives to mitigate the risks associated with financial crimes effectively. Despite challenges posed by evolving regulatory landscapes, cybersecurity threats, and the rapid pace of technological innovation, the UAE remains committed to enhancing its AML capabilities through collaboration, innovation, and continuous adaptation. By fostering cross-border cooperation, investing in advanced technologies, and prioritizing compliance and integrity, the UAE reinforces its position as a global leader in combating money laundering activities. Moving forward, sustained efforts and proactive initiatives will be essential to staying ahead of emerging threats and maintaining the UAE’s reputation as a trusted and secure financial jurisdiction.

FAQs About Anti-Money Laundering (AML) in the UAE

1. What is Anti-Money Laundering (AML)?

Anti-Money Laundering (AML) refers to a set of regulations, laws, and procedures designed to prevent criminals from disguising illegally obtained funds as legitimate income. It aims to deter illicit activities such as drug trafficking, terrorism financing, and corruption.

2. What is the role of the Central Bank of the UAE in AML?

The Central Bank of the UAE serves as the primary regulatory authority overseeing compliance with AML regulations by financial institutions operating within the UAE. It sets guidelines and monitors adherence to AML standards.

3. What are Know Your Customer (KYC) procedures?

KYC procedures require financial institutions to verify the identity of their clients, assess their risk profiles, and obtain information about their business activities to prevent money laundering and financial crimes.

4. What is Customer Due Diligence (CDD)?

Customer Due Diligence (CDD) is a process by which financial institutions assess the integrity of their customers and the legitimacy of their transactions, particularly for high-risk customers such as politically exposed persons (PEPs) and entities operating in high-risk jurisdictions.

5. What are the penalties for non-compliance with AML regulations in the UAE?

Non-compliance with AML regulations in the UAE can result in severe penalties, including fines, license revocation, and legal sanctions for individuals and entities found guilty of money laundering offenses.

6. How does transaction monitoring work in AML?

Transaction monitoring involves the use of sophisticated systems and algorithms by financial institutions to analyze customer transactions in real-time, flagging any unusual or suspicious activities for further investigation to prevent money laundering.

7. What is the role of the Financial Intelligence Unit (FIU) in the UAE?

The Financial Intelligence Unit (FIU), operating under the UAE Ministry of Justice, receives and analyzes suspicious transaction reports from financial institutions, enhancing the country’s ability to detect and combat money laundering activities.

8. How does the UAE collaborate internationally in AML efforts?

The UAE actively participates in international initiatives and collaborates with organizations such as the Financial Action Task Force (FATF) to strengthen its AML framework, exchange financial intelligence, and enhance cooperation with foreign counterparts.

9. What technological innovations are used in AML in the UAE?

The UAE leverages technological advancements such as artificial intelligence (AI), machine learning, data analytics, and blockchain technology to enhance AML detection capabilities, improve transaction transparency, and mitigate risks associated with financial crimes.

10. What are some challenges faced in AML efforts in the UAE?

Challenges in AML efforts in the UAE include evolving regulatory requirements, cybersecurity risks, the emergence of new technologies, and the need for enhanced cross-border collaboration to effectively combat money laundering activities.

11. How do financial institutions ensure compliance with AML regulations?

Financial institutions in the UAE ensure compliance with AML regulations through stringent adherence to regulatory requirements, implementation of KYC and CDD procedures, transaction monitoring, employee training, and investments in technology and compliance infrastructure.

12. What is the regulatory framework for AML in the UAE?

The regulatory framework for AML in the UAE includes Federal Decree-Law No. 20 of 2018 concerning anti-money laundering and combating the financing of terrorism (AML/CFT), which outlines the obligations and responsibilities of entities operating within the UAE’s financial sector.

13. How does the UAE address cyber-enabled money laundering?

The UAE addresses cyber-enabled money laundering by investing in robust cybersecurity infrastructure, implementing stringent protocols, and leveraging advanced technologies to safeguard against cyber threats and prevent illicit financial activities.

14. What is the importance of training and awareness programs in AML?

Training and awareness programs are essential in AML efforts to equip employees with the knowledge and skills necessary to identify, prevent, and report potential money laundering activities, thus strengthening overall compliance and integrity within financial institutions.

15. How can individuals and businesses contribute to AML efforts in the UAE?

Individuals and businesses can contribute to AML efforts in the UAE by adhering to regulatory requirements, conducting due diligence on their clients and transactions, reporting suspicious activities to authorities, and staying informed about AML developments and best practices.

For example, your year end close becomes a lot simpler if you have accurate monthly reports to work from. To learn more about exactly which taxes your tax-exempt nonprofit might still be on the hook for, consult IRS Publication 557, or better yet, consult with a nonprofit tax specialist. They’ll have experience helping organizations like yours minimize their tax bill and make sure you aren’t breaking any tax code rules. This is essentially the nonprofit accounting version of the balance sheet equation. Once you’ve got a bookkeeping system in place, you need to start creating financial statements.

Just like the statement of financial position, the statement of activities keeps net assets that have conditions and stipulations attached to them separate from unrestricted funds. As you come to the end of your accounting year, you need to wrap up your books for the previous year and start the books for the next year. Your accounting period indicated the beginning and end of your reporting period, which can be 6, 12, or 18 months, depending on the needs of your nonprofit. If you choose the most common reporting period of 12 months, this period can be a calendar year (January to December) or a fiscal year (using another 12-month period).

FASB Clarifies and Improves Guidance for Not-for-Profit Grant and Contribution Accounting

Most organizations don’t bother with accruing payroll until fiscal year end, but other than that, it’s a good idea to adjust most other balance sheet accounts each month. It goes without saying that you should never use your personal bank account for your nonprofit organization. You can always ask your bank about your account options and use those tailored for nonprofits. If you’re looking for a one-stop-shop online fundraising tool that seamlessly integrates with your CRM, marketing tool, or accounting software, take a look at Donorbox. Over 80,000 nonprofits worldwide have used our tool to boost donations with features like peer-to-peer fundraising, text-to-give, event ticketing, recurring donations, and more. A bookkeeper with experience in fund accounting will create detailed fund accounting reports to help your accountant file quarterly statements and perform audits.

For the most part, nonprofits can apply to the IRS to become exempt from federal taxes under Section 501. For the most part, however, cash flow statements for non and for-profits are very similar. If you’ve dealt with for-profit cash flow statements before, this should look very familiar. You probably didn’t start a nonprofit organization to stare at spreadsheets and Google things like “how to record an in-kind donation.” It may be hard to believe but getting too much money can sometimes destabilize a nonprofit organization.

How to set up bookkeeping for your nonprofit

While you can certainly buy a ledger book at an office supply store, keep in mind that it’s much easier to set up your chart of accounts if you’re using an accounting software, such as Wave. Run annual reports to check for accuracy and make sure all accounts balance. Make sure to adjust entries as needed, and then re-run the reports and print them for your records. To ensure that happens, your accounting department and finance team need to work together to create a month end close process. Looking up a nonprofit’s Form 990—using services like Guidestar.org—can tell you a lot about its financial state.

As mentioned above, you’ll want to review and make any needed changes to your employees’ W-4 Forms. In addition to this, be sure to send contribution statements and a Form 1099 for vendors by January 31. After posting subledger transactions, check for any transactions that may not be complete. Break year-end close tasks into assignments with due dates and monitor real-time status including tracking the percentage completion for each assignment. In this way, Sage Intacct makes it easy to customize reporting while maintaining a streamlined chart of accounts. According to the Close the Books survey, finance teams that adopt a cloud financial accounting solution are on average 25% more automated than those using an on-premises solution.

Record Incoming Cash

You’ll see how Aplos can help simplify your bookkeeping so you can spend less time doing administrative work and more time focusing on your mission. No matter where the cash comes from, you need to have a record of it. That means verifying that you’ve sent invoices and cross-checking which invoices clients have paid. Furthermore, review your general ledger to ensure you’ve posted credit and debit entries correctly.

Sage Intacct has a table-driven chart of accounts, which lets you create primary natural account codes (assets, liabilities, net assets, revenues, and expenses). You can also tag transactions with attributes bookkeeping for nonprofits called “dimensions” (location, grant, fund, program, and more) that provide additional context. During any given month, you track expenses, income, donors, fund balances, bank transfers, and more.

Economic Substance Regulation (ESR) has emerged as a pivotal tool in combatting tax evasion and ensuring fair taxation in the global economy. It addresses concerns regarding base erosion and profit shifting (BEPS), where multinational corporations exploit tax loopholes to minimize tax liabilities. ESR mandates that entities demonstrate genuine economic activities in jurisdictions where they operate, emphasizing substance over form. Compliance with ESR requires businesses to align their operations with core income-generating activities, maintain a physical presence, and centralize management functions in relevant jurisdictions.

Implementing ESR entails increased transparency, accountability, and compliance costs for businesses. However, it also fosters fair competition and tax fairness. Future trends in ESR point towards harmonization, strengthened enforcement, and the adoption of technological solutions to enhance compliance and enforcement efforts.

Overall, ESR represents a paradigm shift in global tax governance, aiming to ensure that businesses contribute their fair share of taxes in jurisdictions where they generate profits. As ESR frameworks continue to evolve, businesses must remain proactive in their compliance efforts to navigate the complexities of global taxation successfully.

Understanding Economic Substance Regulation

In today’s globalized economy, nations strive to ensure fair taxation and prevent the abuse of their tax systems. One of the tools utilized for this purpose is Economic Substance Regulation (ESR). ESR refers to a set of rules and requirements imposed by tax authorities to ensure that entities conducting business within their jurisdiction have substantial economic activities and genuine business operations, rather than merely serving as conduits for tax evasion or avoidance.

The Origins of Economic Substance Regulation

ESR gained prominence in response to concerns about base erosion and profit shifting (BEPS), a phenomenon where multinational corporations exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax jurisdictions. This practice deprives countries of legitimate tax revenues and distorts fair competition among businesses.

Key Objectives of Economic Substance Regulation

Combat Tax Avoidance: ESR aims to prevent tax evasion and aggressive tax planning strategies employed by entities to reduce their tax liabilities artificially.

Promote Transparency: By requiring entities to demonstrate genuine economic activity in the jurisdictions where they operate, ESR promotes transparency and accountability in tax matters.

Ensure Fair Taxation: ESR seeks to ensure that businesses pay taxes where they generate profits, thus fostering fair taxation and preventing the erosion of tax bases.

Implementing Economic Substance Regulations

ESR frameworks vary from one jurisdiction to another, but they generally include criteria that entities must meet to demonstrate economic substance. These criteria typically revolve around the nature and extent of the entity’s operations, including:

Core Income-Generating Activities (CIGAs): Entities are required to conduct substantial CIGAs within the jurisdiction, aligning with the nature of their business activities.

Presence of Adequate People and Assets: ESR often mandates that entities have an adequate number of qualified employees and physical assets proportionate to their business activities.

Management and Control: Entities must demonstrate that strategic decisions are made locally and that key management functions are performed within the jurisdiction.

Implications of Non-Compliance

Non-compliance with ESR can have significant repercussions for businesses. Tax authorities may impose penalties, deny tax deductions, or even disregard transactions conducted by non-compliant entities. In extreme cases, entities may face the risk of being struck off the register or losing their tax residency status.

Global Cooperation and Standardization

Recognizing the cross-border nature of tax evasion, many jurisdictions have embraced international cooperation and adopted standardized approaches to ESR. Initiatives such as the OECD’s BEPS Action Plan and the EU’s Code of Conduct Group on Business Taxation aim to promote consistency and coordination in implementing ESR across jurisdictions.

Requirements and Compliance Strategies

Understanding the Requirements

To comply with Economic Substance Regulation, businesses must understand the specific requirements set forth by the jurisdictions in which they operate. While the nuances may vary, certain core principles typically guide ESR compliance efforts:

Substance over Form

ESR emphasizes substance over form, meaning that entities must demonstrate genuine economic activities and value creation in the jurisdictions where they operate. Merely establishing a shell company or engaging in artificial arrangements to minimize tax liabilities is insufficient to meet ESR requirements.

Alignment with Business Activities

Entities must align their activities with the core income-generating functions relevant to their business. For example, a manufacturing company should have substantial operations related to manufacturing activities within the jurisdiction, such as production facilities and skilled workforce.

Adequate People and Assets

ESR often mandates the presence of an adequate number of qualified employees and physical assets proportionate to the scale and complexity of the business operations. This ensures that entities have the necessary resources to carry out their activities effectively.

Compliance Strategies

Achieving compliance with Economic Substance Regulation requires proactive measures and strategic planning. Here are some key strategies that businesses can adopt:

Conduct a Comprehensive Assessment

Begin by conducting a thorough assessment of your business operations and identifying areas where ESR compliance may be lacking. This includes reviewing the nature and extent of your activities, as well as the presence of necessary resources and management functions.

Establish Substance in Relevant Jurisdictions

Ensure that your business has a genuine presence and conducts substantial activities in jurisdictions where you operate. This may involve establishing physical offices or facilities, hiring local employees, and engaging in meaningful business operations.

Centralize Management and Control

Centralize key management functions and decision-making processes within jurisdictions where your business has a significant economic presence. This helps demonstrate that strategic decisions are made locally and align with the substance of your operations.

Maintain Detailed Records

Keep comprehensive records documenting your business activities, expenditures, and decision-making processes. This not only facilitates compliance with ESR requirements but also serves as evidence in the event of an audit or inquiry by tax authorities.

Stay Informed and Adapt

Stay abreast of developments in ESR frameworks and regulations in relevant jurisdictions, as they may evolve over time. Adapt your compliance strategies accordingly to ensure ongoing adherence to emerging standards and requirements.

Implications and Future Trends

Broader Implications of Economic Substance Regulation

The implementation of Economic Substance Regulation has far-reaching implications for global taxation and business practices. Some of the key implications include:

Enhanced Tax Transparency

ESR promotes greater tax transparency by requiring entities to disclose detailed information about their business activities and operations. This transparency helps tax authorities assess the legitimacy of transactions and combat tax evasion more effectively.

Shift in Business Strategies

Businesses may need to reconsider their international tax planning strategies in light of ESR requirements. Traditional tax optimization structures that rely heavily on low-tax jurisdictions may no longer be viable, prompting businesses to explore alternative approaches that prioritize genuine economic substance.

Increased Compliance Costs

Complying with ESR entails additional administrative burdens and compliance costs for businesses. From conducting comprehensive assessments to maintaining detailed records and implementing compliance measures, businesses must allocate resources to ensure adherence to ESR requirements.

Future Trends in Economic Substance Regulation

As Economic Substance Regulation continues to evolve, several trends are shaping its future trajectory:

Harmonization and Standardization

There is a growing trend towards harmonizing and standardizing ESR frameworks across jurisdictions. International initiatives such as the OECD’s BEPS Action Plan and the EU’s Code of Conduct Group on Business Taxation aim to promote consistency and coordination in implementing ESR, reducing compliance complexities for businesses operating across borders.

Strengthened Enforcement

Tax authorities are increasingly focused on enforcing ESR requirements and combating tax evasion and avoidance. This may involve enhanced monitoring, audits, and penalties for non-compliant entities, incentivizing businesses to prioritize compliance efforts.

Technological Solutions

Advancements in technology, such as blockchain and data analytics, are being leveraged to enhance ESR compliance and enforcement. These technologies enable real-time monitoring of transactions and facilitate the analysis of large volumes of data to identify non-compliance risks more efficiently.

Economic Substance Regulation (ESR) marks a significant milestone in global tax governance, signaling a shift towards transparency, fairness, and accountability. By requiring entities to demonstrate genuine economic activities in the jurisdictions where they operate, ESR aims to combat tax evasion, promote tax transparency, and ensure fair taxation. Compliance with ESR entails proactive measures, including aligning business activities with core income-generating functions, maintaining physical presence, and centralizing management functions.

While compliance with ESR may incur additional costs for businesses, the benefits of enhanced tax transparency and fair competition outweigh the challenges. As ESR frameworks evolve and adapt to changing economic landscapes, businesses must remain vigilant and proactive in their compliance efforts to navigate the complexities of global taxation successfully.

Ultimately, ESR represents a collaborative effort among policymakers, tax authorities, and businesses to create a more equitable and sustainable tax environment. By embracing the principles of transparency and accountability, ESR paves the way for a fairer and more inclusive global economy.

FAQs:

What is Economic Substance Regulation (ESR)?

Economic Substance Regulation (ESR) refers to a set of rules and requirements imposed by tax authorities to ensure that entities conducting business within their jurisdiction have substantial economic activities and genuine business operations.

Why was Economic Substance Regulation introduced?

ESR was introduced to address concerns about base erosion and profit shifting (BEPS), where multinational corporations exploit tax loopholes to minimize tax liabilities, depriving countries of legitimate tax revenues.

Which jurisdictions have implemented Economic Substance Regulation?

Various jurisdictions, including offshore financial centers and major economies like the EU member states, have implemented Economic Substance Regulation to combat tax evasion and ensure fair taxation.

What are Core Income-Generating Activities (CIGAs) under ESR?

Core Income-Generating Activities (CIGAs) are the key operational activities that generate income for an entity. Under ESR, entities are required to conduct substantial CIGAs within the jurisdiction where they operate to demonstrate economic substance.

What are the penalties for non-compliance with Economic Substance Regulation?

Penalties for non-compliance with ESR may include fines, denial of tax deductions, or even the loss of tax residency status for entities. Tax authorities may also disregard transactions conducted by non-compliant entities.

How can businesses ensure compliance with Economic Substance Regulation?

Businesses can ensure compliance with ESR by aligning their operations with core income-generating activities, maintaining a physical presence in relevant jurisdictions, and centralizing management functions locally.

Are there any exemptions or exceptions to Economic Substance Regulation?

Some jurisdictions may provide exemptions or exceptions to certain types of entities or activities under ESR. However, these exemptions are typically limited and subject to specific conditions.

How often do businesses need to report their compliance with Economic Substance Regulation?

Reporting requirements for compliance with ESR vary depending on the jurisdiction. Businesses may need to report their compliance annually or as required by tax authorities.

What documentation is required to demonstrate compliance with Economic Substance Regulation?

Documentation required to demonstrate compliance with ESR may include records of business activities, expenditures, decision-making processes, and details of physical presence and staffing.

What are the potential risks of non-compliance with Economic Substance Regulation?

Non-compliance with ESR can expose businesses to various risks, including reputational damage, financial penalties, and legal consequences. It may also impact the entity’s ability to conduct business internationally.

How do international organizations like the OECD contribute to Economic Substance Regulation?

International organizations like the OECD play a significant role in promoting consistency and coordination in the implementation of ESR across jurisdictions. They develop guidelines and best practices to assist countries in implementing effective ESR frameworks.

Can businesses outsource certain activities to comply with Economic Substance Regulation?

While outsourcing certain activities may be permissible under ESR, businesses must ensure that outsourced activities contribute to the economic substance of the entity and are conducted in compliance with relevant regulations.

How does Economic Substance Regulation impact cross-border transactions?

ESR may impact cross-border transactions by requiring entities to demonstrate economic substance in jurisdictions where they operate. This may influence the structuring of transactions and tax planning strategies.

Are there any industry-specific guidelines or regulations related to Economic Substance Regulation?

Some industries may have specific guidelines or regulations related to ESR compliance. Businesses operating in regulated industries should be aware of any industry-specific requirements that may apply to them.

How can businesses stay informed about changes and updates to Economic Substance Regulation?

Businesses can stay informed about changes and updates to ESR by monitoring regulatory developments, seeking guidance from tax advisors, and participating in industry forums and discussions. It’s essential to remain proactive and adaptable to evolving regulatory landscapes.